by Mike O'Boyle* Offshore wind may seem like a pricey option, but it’s actually an extremely valuable investment. A new analysis from the Lawrence Berkeley National Laboratory (LBNL) shows that the market value of electricity generated by offshore wind will soon exceed its cost in New York and several New England states

Offshore wind may seem like a pricey option, but it’s actually an extremely valuable investment. A new analysis from the Lawrence Berkeley National Laboratory (LBNL) shows that the market value of electricity generated by offshore wind will soon exceed its cost in New York and several New England states.

The economic impact of offshore wind is even more significant after adding in the tens of thousands in new jobs and billions in new investment that come from steel in the water. Massachusetts, Maryland, and New York are already accelerating offshore wind’s expansion, and states like New Jersey aren’t far behind in a race to the top.

Even the Trump Administration is touting offshore wind’s upside. "As we look to the future, wind energy – particularly offshore wind – will play a greater role in sustaining American energy dominance,” wrote Interior Secretary Ryan Zinke. "Offshore wind uniquely leverages the natural resource off of our East Coast, bringing jobs and meeting the region’s demand for renewable energy.”

Offshore wind’s attractive East Coast economic attributes

On a levelized cost of energy basis, offshore wind still seems more expensive than more ubiquitous onshore wind and solar, but when and where power is generated matters a great deal for whether generators provide value to buyers. LBNL’s new analysis shows that high capacity factors of offshore wind, the coincidence of wind with customer demand, and potential locations adjacent to congested coastal load centers like New York City and Boston already make offshore wind an economic option.

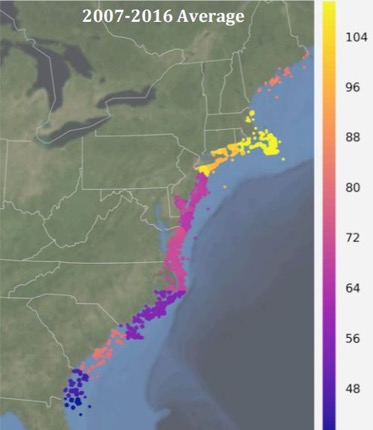

LBNL quantifies the value of offshore wind by adding the energy, capacity, and renewable energy certificate (REC) revenues power plants could expect by participating in each market. When averaged over the entire 2007-2016 period, LBNL found the median marginal value for offshore wind sites connecting to New England’s ISO-NE grid is roughly $110 per megawatt-hour (MWh), compared to $100/MWh for sites interconnecting to New York’s NYISO grid, $70/MWh for sites in the Mid-Atlantic’s PJM Interconnection grid, and closer to $55/MWh for sites in the non-competitive Southeast.

Total offshore wind market value at each site averaged over 2007-2016.

$110-100/MWh values in the Northeast already approach near- to medium-term anticipated all-in costs to build offshore wind, evidenced by recent auction results. Maryland paid $132/MWh REC prices for 386 megawatts (MW) of offshore wind capacity in 2017 to come online in 2020, down from over $250/MWh paid for Rhode Island’s 30 MW Block Island offshore wind farm, which came online in 2016.

Much larger offshore wind auctions are on the horizon, with nearly 8,000 MW of offshore wind procurement announced by state governments in the Northeast U.S. By the time Europe reached that capacity figure, offshore wind contracts were being signed for $80/MWh or less, and that was with inferior technology, i.e. smaller turbines.

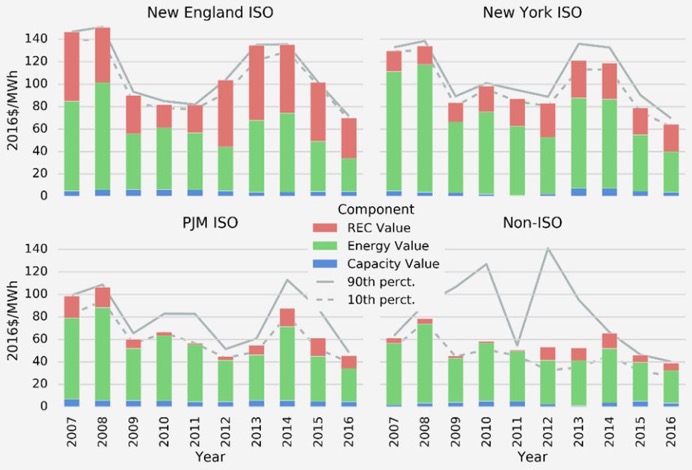

Median energy, capacity, REC value by year for offshore wind sites within each region.

Offshore wind’s extreme value in Northeast states shouldn’t come as a surprise. Higher REC prices primarily drive LBNL’s finding, but energy prices are also higher in New England and New York than in PJM and the Southeast U.S. These high REC prices derive from difficulty siting projects on the most constrained land in the U.S. and relatively lackluster onshore wind and solar resources, combined with some of America’s most ambitious renewable energy goals, which on average will require the region to hit 40% renewables by 2030.

LBNL found that offshore wind prevents the most emissions of carbon dioxide and other pollutants in the Mid-Atlantic PJM region, mostly due to the higher emissions intensity of the generators running in that market

It’s remarkable that with just 30 MW of installed capacity, the U.S. is close to offshore wind turbines being in the black. Falling wholesale market electricity prices, driven by a glut of cheap gas and excess coal and nuclear generation that could soon retire due to economic pressure, have undercut this value proposition, but that could very well rebound as excess supply retires.

Ancillary environmental and consumer cost benefits

Depending on how fast costs fall, cheaper offshore wind could even keep regional electricity prices low for some time to come, creating additional consumer benefits. LBNL also quantifies the potential environmental and economic benefits of offshore wind, finding offshore wind significantly reduces air pollution and reduces natural gas and energy prices – to consumers’ benefit.

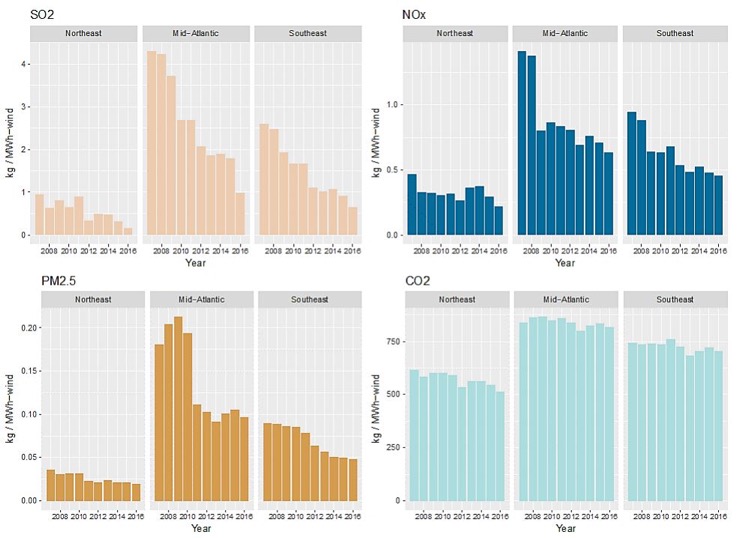

Avoided SO2, NOx, PM2.5, and CO2 emissions rate by year for average offshore wind profile in each region.

LBNL found that offshore wind prevents the most emissions of carbon dioxide and other pollutants in the Mid-Atlantic PJM region, mostly due to the higher emissions intensity of the generators running in that market. By their measure, 1 MWh of offshore wind avoids 800 kilograms (kg) of carbon emissions.

But 800kg/MWh is a bit hard to understand, so let’s take a deeper look at how this applies in practice. Maryland’s 2017 offshore wind solicitation procured the 120 MW Skipjack offshore wind farm, with an implied capacity factor (i.e., how much it produces relative to its maximum theoretical output) of 43%.

Because offshore wind bids into a wholesale market at zero marginal cost, it would also reduce wholesale energy prices and demand for natural gas, which has a marginal fuel cost, thereby reducing gas and electricity costs to customers

Applying this avoided emissions rate around 800kg/MWh, which is what you would see if Skipjack sells its power into PJM, the 120 MW wind farm would avoid 364,000 metric tons of CO2 annually – that’s about equal to the emissions of 80,000 passenger vehicles.

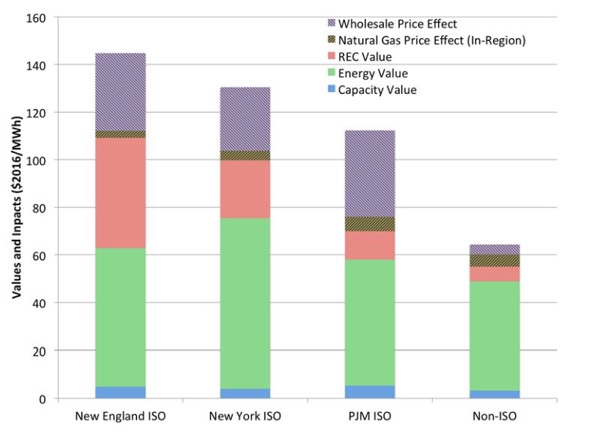

Because offshore wind bids into a wholesale market at zero marginal cost, it would also reduce wholesale energy prices and demand for natural gas, which has a marginal fuel cost, thereby reducing gas and electricity costs to customers. LBNL calculates these "merit order effects” at $6/MWh for natural gas prices, and $25/MWh in wholesale energy costs in wholesale market regions. The savings are significantly lower in the states south of the PJM region.

Median energy, capacity, and REC value along with the in-region natural gas price effect and wholesale electricity price effect averaged over 2007-2016.

Evidence is also growing that offshore wind will create tens of thousands of jobs in the Northeast. Combining existing contracts with New Jersey’s 3,500 MW goal, New York’s 2,400 MW goal, and Massachusetts’ 1,600 MW goal, the regional market would reach at least 8,000 MW by 2030.

The Northeast Wind Center projects this would create 36,300 full-time jobs, while New York expects a $6 billion in-state industry by 2028, and Massachusetts projects up to $800 million in direct economic impacts along with up to 3,170 job years from offshore wind in the next decade.

Massachusetts is already reaping dividends from its offshore wind goal. Three coastal communities that have suffered economically from manufacturing and fishing industry declines are in the final running for developer Deepwater Wind’s new wind turbine assembly facility and its 900 new jobs. In addition, the retired Brayton Point coal plant was recently acquired by a real-estate developer with plans to turn it into a construction hub for planned offshore wind farms and connection point to the regional grid once projects begin operation.

Levelized cost of energy doesn’t always tell the whole story

The levelized cost of energy, though a valuable metric for comparing different technologies, fails to tell the whole story of the value of energy. Offshore wind is more valuable in Northeast states where renewables’ policy value combines with higher wholesale energy prices to create a more attractive market than in the Mid-Atlantic and Southeast regions.

Couple this with the industry’s history of rapid cost declines and regional demand for clean energy, and it’s easy to see a bright future for offshore wind developers in the near to medium term – along with billions in upside for the states who embrace offshore wind’s economic potential.

*Mike O’Boyle is Energy Innovation’s Electricity Policy Manager and Project Manager at America’s Power Plan.

(Forbes.com/ energypost.eu, May 25, 2018)